The Ultimate Guide to Property Management Trust Accounting

October 29, 2025

Quick Summary

Trust accounting is one of the most important and most misunderstood parts of property management. This guide explains how it works, why state laws treat client funds differently, and what every manager must do to stay compliant. From opening the right kind of trust account to reconciling it correctly, you’ll learn the best practices that protect your business, your clients, and your reputation.

Are You Managing Client Money the Way the Law Expects You To?

The law is clear: the rent you collect and the fees you earn are never meant to mix. And that’s why property managers are required to maintain a trust account — one that keeps client money separate, traceable, and fully accountable.

Still, for something so essential, trust accounting can feel unnecessarily complicated. Some banks don’t know what kind of account you’re asking for. State laws read differently everywhere you look. And some software meant to make life easier simply isn’t built to handle compliance properly.

That’s why we’ve written this guide to simplify everything. We’ll explain what trust accounting means, how to set it up correctly, how different laws come into play, and how to manage it confidently without fear of getting it wrong.

Why Listen to Us

At Revela, we’ve seen how complicated trust accounting can get with missed reconciliations, messy audits, and strict compliance rules.

We built Revela to fix that. Our software automates reconciliations, enforces trust rules, and keeps every dollar where it belongs so you stay compliant and confident.

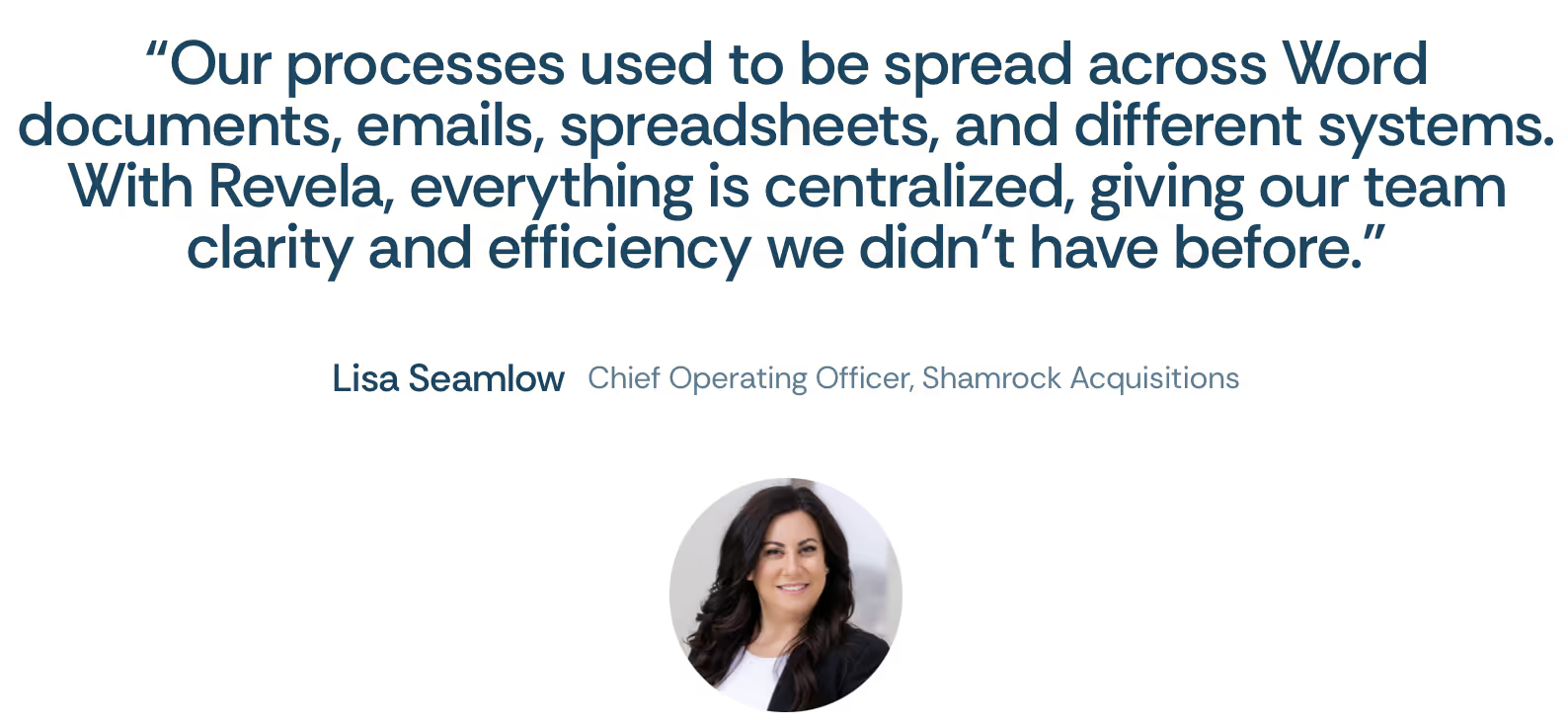

Here’s what one of our clients has to say:

This guide walks you through the same standards and best practices our platform was built to support.

What Is Trust Accounting?

Trust accounting is the process of managing money that does not belong to you. It covers client funds such as rent, owner payments, and security deposits, and ensures that every dollar is kept separate, traceable, and compliant with the law.

As a property manager, you are required to hold this money in a trust account, which is a dedicated bank account used only for client funds. You act as a fiduciary, which means you have a legal and ethical duty to manage those funds responsibly without mixing them with your own business finances.

Here is what that looks like in practice.

A tenant pays $2,000 in rent. It does not go into your operating account. It first lands in your trust account, where $1,800 might be disbursed to the property owner, $100 goes to a repair vendor, and your $100 management fee is transferred only after reconciliation. Each transaction is recorded, and every dollar can be traced back to a specific property and client.

Trust accounting aims to protect all parties involved. It provides a clear record of how client money moves, helps prevent misuse or errors, and shows that every transaction is handled with integrity and transparency.

The Tricky Part of Setting Up a Trust Account

The process of setting up a trust account is where many property managers run into problems.

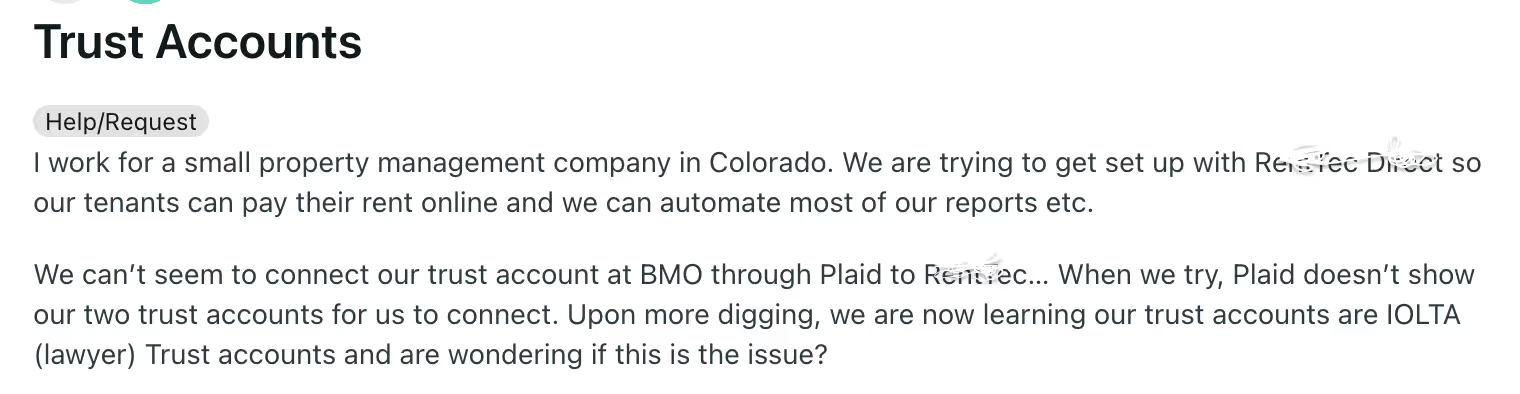

We have seen several managers online share their frustrations about opening a trust account. Many say their banks do not understand what they are asking for.

Others are handed the wrong type of account, often an IOLTA or family trust account, which their property management software cannot connect to or recognize. Here’s one of them sharing their experience.

The confusion happens because not all banks understand property management trust accounts, and the rules for setting them up vary from state to state.

For example, in Colorado, trust accounts are treated as fiduciary accounts under the Division of Real Estate. The state requires property managers to keep client funds and security deposits in separate accounts and to perform monthly reconciliations. You can even find a list of banks familiar with this setup on the state’s official website. But in other states, such as California, both client and security deposit funds can be held in one trust account as long as records clearly separate them.

Because these laws differ across the U.S., property managers must pay attention to both state regulations and bank capabilities before opening any account. Not every financial institution offers the correct structure for trust accounting.

How to Set Up a Trust Account the Right Way

Once you understand how complex the process can be, the next step is making sure you set it up correctly. Doing it right from the start prevents most compliance issues later and ensures your bank, your software, and your systems all work together.

Here are a few general guidelines to follow when setting up a property management trust account:

- Use precise language when you visit the bank: Ask for a Property Management Trust Account or a Real Estate Broker Trust Account.

- Confirm the account is recognized as a fiduciary account: The bank should understand that funds will belong to clients, not you.

- Title the account clearly: Use names like [Your Business Name] – Client Trust Account or [Your Business Name] – Security Deposit Account.

- Verify compatibility with your property management software: Some banks’ systems cannot sync properly with accounting tools, which can cause reconciliation errors.

- Check if the bank is FDIC insured: This ensures deposits are protected up to $250,000 per beneficiary when properly recorded.

Setting up your trust account correctly from the beginning saves you time, prevents compliance mistakes, and builds a clean foundation for everything that follows.

Managing a Trust Account for Accuracy and Compliance

Once your trust account is set up, the real work begins. The goal is not just to keep client money safe but to manage it in a way that is organized, transparent, and always ready for review. With the right system, much of this can happen automatically.

Deposit Funds Promptly

Rent payments, deposits, and owner funds should be deposited as soon as possible, usually within the timeframe your state requires. Some states specify three business days, others five.

Revela can automatically record deposits from online payments and assign them to the correct property and client ledger, removing the need for manual entry.

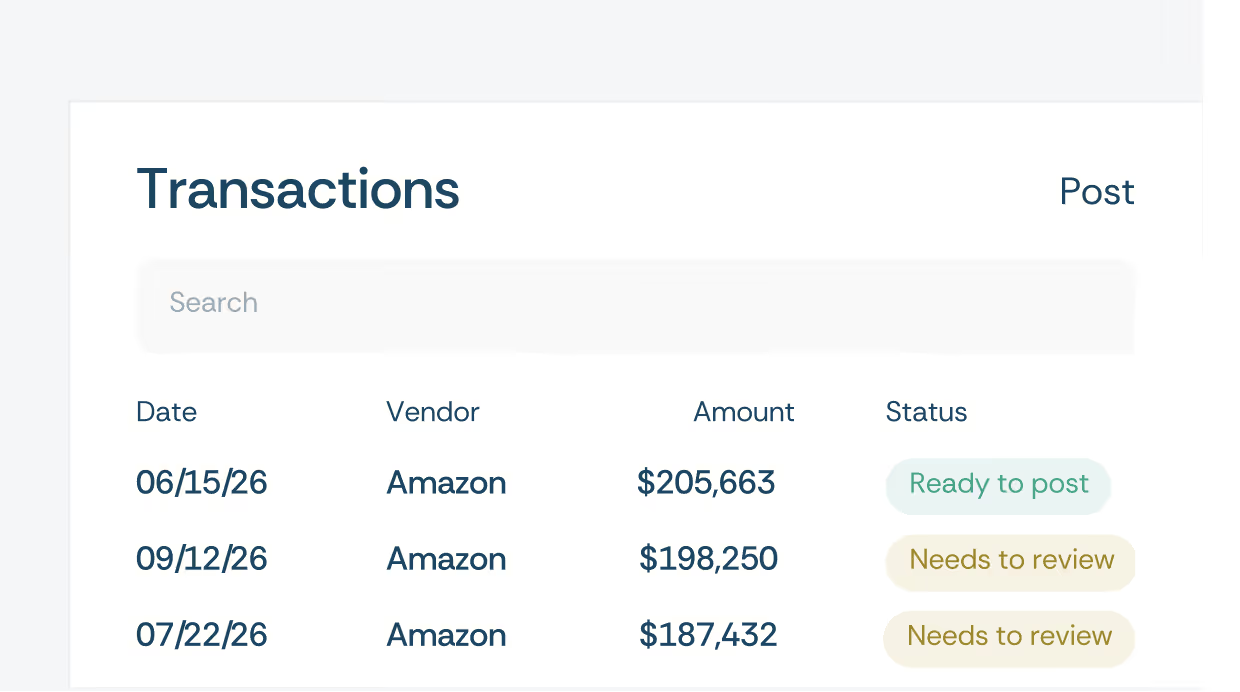

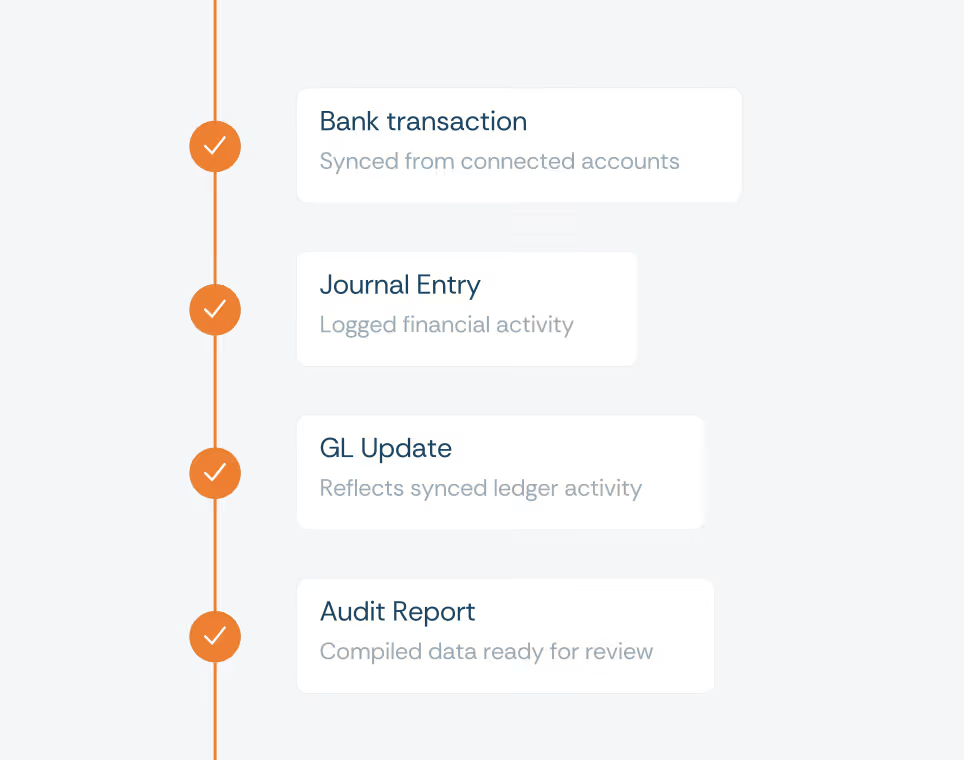

Record Every Transaction Clearly

Each payment and withdrawal should tell a clear story: who the money came from, who it went to, and why. In Revela, this happens automatically. Each transaction is tagged to the right owner or tenant, creating a complete, real-time record that aligns perfectly with your trust account.

Pay Owners and Vendors Carefully

Do not make payments until funds have cleared. Always verify balances before disbursing money to owners, paying vendors, or transferring your management fee. With the Revela’s embedded banking system, you can get a clear visibility into available balances and linked transactions before every disbursement.

Keep Your Management Fees Separate

Management fees should only be moved into your business account after reconciliation. Taking them early, even unintentionally, is considered commingling.

Reconcile Monthly Without Fail

At least once every month, your bank balance, ledger balance, and book balance should all match exactly. This three-way reconciliation is the backbone of compliance. Revela performs this process automatically, comparing your live bank data with your trust ledgers and alerting you if anything does not align.

Keep Records That Defend You

Your records are your best defense during audits or disputes. Keep digital copies of deposit slips, statements, and ledgers organized and easy to retrieve. Revela securely stores all financial records, organizes them by property and date, and makes them exportable for regulators or auditors when needed.

Stay Consistent

The hardest part of trust accounting is not the math but the discipline. Build a simple rhythm and stick to it. Revela supports that rhythm by automating repetitive tasks and giving you visibility into every account, transaction, and balance in one place.

Property Management Trust Accounting Best Practices

Managing a trust account well is one thing. Running a business that stays compliant, audit-ready, and trusted at scale is another. These best practices help you build a system that protects your business long-term.

Create Written Policies and Internal Controls

Document how your company handles client funds from start to finish — deposits, fee transfers, reconciliations, and audits. Written procedures make your workflow consistent and help train new team members quickly and correctly.

Assign Clear Responsibility

Even when automation handles most of the work, someone on your team should still review reconciliations and reports. Clear ownership prevents oversights and strengthens accountability during audits.

Audit Yourself Before the State Does

Do an internal audit at least once a quarter. Review reconciliations, client balances, and disbursement timelines. Revela makes this simple by letting you export reports and trace every transaction by owner or property.

Stay Current with State Regulations

Each state’s rules evolve over time. Bookmark your state’s Real Estate Commission or Department of Regulatory Agencies website and check for updates at least once a year. Revela can help you align your workflows when new requirements appear.

Separate Accounts Strategically

Even if your state allows combined accounts, consider keeping rent and security deposits in different trust accounts. This small step adds clarity and eliminates confusion during audits or owner reviews.

Communicate Frequently with Owners

Regular, transparent communication prevents mistrust. Send owners consistent, itemized statements showing how their funds move. Revela can generate these automatically, reinforcing confidence and professionalism.

Treat Compliance as a Culture

Compliance should not be something you check at the end of the month; it should be part of your daily routine. When accuracy, transparency, and accountability become habits, audits become easy and clients stay loyal.

Frequently Asked Questions

Can I use one trust account for both rent and security deposits?

It depends on your state. Some states, such as California, allow combined accounts as long as records clearly separate client and tenant funds. Others, like Colorado, require separate accounts for security deposits and operating funds.

What happens if I mix business and client money?

Mixing funds, known as commingling, is a serious violation. It can lead to penalties, audits, or even the loss of your license. Keeping clear boundaries between business and client money is essential for compliance.

How do I know if my trust account is FDIC insured?

Ask your bank directly. The account must be titled correctly as a trust or fiduciary account, and your internal records must show how much belongs to each client. When those conditions are met, each client’s funds are insured separately up to $250,000.

Can I open a trust account at any bank?

Not all banks offer the right type of trust account for property management. Some confuse it with a family trust or IOLTA account. If your banker seems unsure, share your state’s trust account requirements or use resources from your real estate commission to confirm eligibility.

How often should I reconcile my trust account?

At least once a month. Regular reconciliation ensures your bank, book, and ledger balances match and helps prevent compliance issues. Tools like Revela can handle this automatically and alert you if anything doesn’t align.

What is the best way to prepare for a state audit?

Stay audit-ready year-round. Keep complete digital records, reconcile monthly, and make sure each transaction is linked to a specific property or client. Revela automatically stores and organizes this documentation for quick access when needed.

How long should I keep trust account records?

Most states require records to be kept for at least three to five years after the end of a transaction or management agreement. Always confirm your state’s specific retention period.

Getting Trust Accounting Right

Trust accounting is about responsibility. Every rent payment, deposit, or disbursement represents someone’s trust in how you manage their money. Getting it right builds credibility with owners, protects your license, and strengthens your business.

The process may be complex, but it does not have to be complicated. With Revela, property managers have a system that keeps trust accounting accurate, compliant, and transparent by default.

Get started with Revela today.